Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,721 million (4.45 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover, and the EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at Ksh 119.09, Ksh 121.31 and Ksh 144.51 respectively. The observed overall depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 5.26% | 0.24% |

| Euro | -5.29% | 0.53% |

| Sterling Pound | -5.14% | 1.02% |

Liquidity

Liquidity in the money markets eased, partly reflecting government payments which offset tax remittances. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 5.47% | 5.25% |

| Interbank volume (billion) | 23.8 | 20.9 |

| Commercial banks’ excess reserves (billion) | 27.2 | 27.4 |

Fixed Income

T-Bills

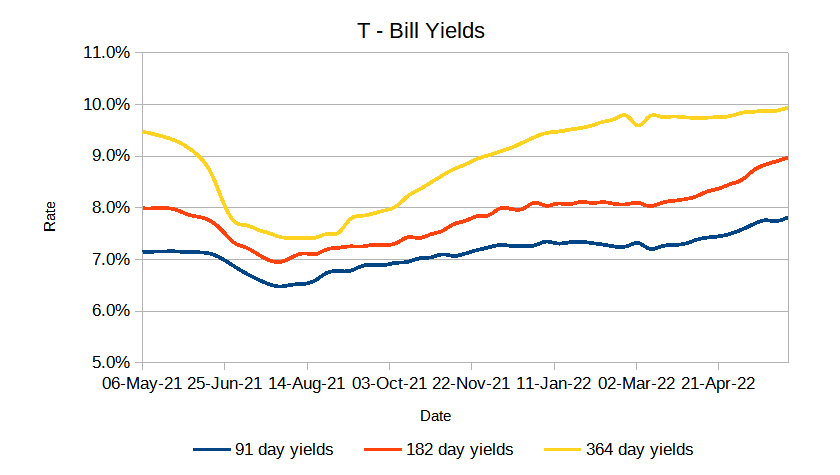

T-Bills were under-subscribed during the week with a decrease in the overall subscription rate from 82.11% recorded in the previous week to 48.27%. The 91-day T-Bill got the highest subscription rate at 186.9% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 20.6% and 20.5% respectively. The acceptance rate increased by 5.68% to close the week at 98.59%.

T-Bonds

The bonds market had a lower demand for the week’s bond offers. Bonds turnover decreased by 32.05% from 5.4B in the previous week to 3.67B. Total bond deals remained unchanged.

In the primary bond market, the Central Bank released results for the two re-opened fifteen year treasury bonds ; FXD2/2013/15 and FXD2/2018/15 each receiving bids worth 5.45B and 5.12B respectively.

Eurobonds

In the international market, the yields on the 10-year Eurobonds for Angola decreased and increased for Ghana. Yields on Kenya’s Eurobonds generally decreased by 78.2 basis points compared to the previous week, 0.335% and 8.173% month to date and year to date respectively. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 10.92% | -1.61% | -1.59% |

| 2018 10-Year Issue | 8.98% | 0.14% | -0.48% |

| 2018 30-Year Issue | 5.26% | -0.40% | -0.60% |

| 2019 7-Year Issue | 10.56% | 0.02% | -0.79% |

| 2019 12-Year Issue | 7.27% | 0.17% | -0.41% |

| 2021 12-Year Issue | 6.05% | -0.34% | -0.83% |

Equities

NASI, NSE 20 and NSE 25 increased by 3.98%, 2.99% and 4.68% compared to last week bringing the year to date performance to -15.01%, -9.80% and -12.17% respectively. The market capitalization increased by 0.68% from the previous week to close at 2.213 trillion recording a year to date decline of -14.97%. The performance was driven by gains recorded by large-cap stocks. Top gains were recorded in East Africa Breweries, KCB ,Equity Group and Co-operative Bank which increased by 8.19%, 6.88%, 6.67% and 5.78% respectively.

The Banking sector had shares worth Ksh 567M transacted which accounted for 35.03% of the week’s traded value, Manufacturing & Allied sector had shares worth Ksh 221M transacted which represented 13.68% and Safaricom, with shares worth Kshs 711M transacted represented 43.91% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Uchumi supermarket | 4.35% | 14.29% |

| Bamburi cement | -2.36% | 12.69% |

| Express Kenya | -14.63% | 8.02% |

| Crown paints Ltd | 40.16% | 7.41% |

| Trans Century plc | 0.00% | 7.14% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| Sameer Africa | 24.56% | -10.58% |

| TPS Eastern Africa | 0.33% | -10.00% |

| B.O.C Kenya | 4.64% | -8.44% |

| Kapchorua Tea | 0.75% | -7.18% |

| Nairobi Business Ventures | -40.49% | -4.79% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.35 | 0.41 | 16.96% |

| Derivatives Contracts | 12 | 13 | 8.33% |

| I-REIT Turnover | 0.43 | 0.028 | -93.52% |

| I-REIT Deals | 9 | 3 | -66.67% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -13.58% | 0.36% |

| Dow Jones Industrial Average (DJI) | -10.34% | -0.14% |

| FTSE 100 (FTSE) | -0.87% | 0.22% |

| STOXX Europe 600 | -11.08% | -0.59% |

| Shanghai Composite (SSEC) | -11.16% | -0.81% |

| MSCI Emerging Markets | -18.70% | 0.91% |

| MSCI World Index | -15.10% | 0.21% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -20.67% | 0.75% |

| JSE All Share | -5.84% | 1.02% |

| NSE All Share (NGSE) | 17.89% | 0.70% |

| DSEI (Tanzania) | 0.69% | 0.31% |

| ALSIUG (Uganda) | -7.75% | 4.30% |

U.S stocks closed the week mixed as they recovered some of their early losses after a much stronger than expected July jobs report showed that U.S employers hired far more workers than expected in July raising alarms that the Federal Reserve would continue hiking the interest rates. The central bank policy makers are set to meet later during the month at an annual conference then have their policy meeting in September where they will have a chance to look more into the economic data including inflation.

European stocks closed the week lower after a stronger than expected U.S jobs reported up bets of another 75 basis points rate hike by the Federal Reserve next month with fears of a darkening growth outlook pushing shares towards weekly losses. The Pan-European STOXX 600 lost 0.6%, snapping two weeks positive on worries over harsh economic data from the region, rising geopolitical tensions and fears that the higher interest rates could tip the economy into a recession.

Asia Pacific stocks closed the week higher after recovering some of their losses earlier on in the week. Chinese stocks rose slightly with the Shanghai Shenzhen CSI 300 adding 0.3%. Taiwan, China, Asian and Hong Kong were mostly up at the end of the week with Philippine ending the week low.

On the global commodities markets, Crude Oil WTI closed the week lower by 9.81% and the ICE Brent Crude decreased by 8.37%. Gold futures prices increased by 0.01% to settle at $1,791.20.

Week’s Highlights

- The government extended duty-free maize imports by two more months to allow importers ship in the cereal in a bid to ease the shortage being experienced in the market. The National Treasury opened a 3-month window for importers to bring in up to 540,000 metric tonnes of duty-free maize. This comes at a time the price of maize was subsidized to Ksh 100 up from Ksh 210 for a 2-kilogram of maize flour.

- The Kenyan banking sector registered the highest tax contribution in five years paying a total of Ksh 129.52 billion to the Kenya Revenue Authority in 2021, a 24% increase from Ksh 104.8 billion in 2020. It also recorded a 58% year-on-year increase in excise duty which attributed the growth to the economic recovery in the country.

- Tea worth Ksh 438 million was withdrawn from the market as the price of the beverage continues to tumble with the price dropping to Ksh 261 a kilogram from Ksh 264 a kilogram last week with the decline being attributed to diminishing demand in the market. The low prices saw dealers withdraw 3.6 million kilograms of tea from the auction to trade it in the next sale should prices be in their favour.

- Dividend payout by companies listed on the Nairobi Securities Exchange (NSE) rose to a record sh 130.3 billion, a 53.5% jump from the total payout of Ksh 84.9 billion a year earlier. The latest full year payouts indicate that the entire market currently valued at Ksh 2.18 trillion, has a divided yield of about 6% with the cash ratio being weighed down by scores of firms that have not paid dividends.

- The Zambian Kwacha strengthened after the country’s official creditors agreed to provide financing assurances the nation needs to secure the final approval from the International Monetary Fund (IMF) for a $1.3 billion bail out. The country’s $1 billion Eurobonds due in 2024 advanced for ten straight days rising as much as 0.3% to 6.09 cents on the Dollar. This comes just after Zimbabwe introduced gold coins into the market aimed at battling a resurgence in inflation and depreciation of the Zimbabwean Dollar.

- Kenya and the United Arab Emirates (UAE) announced plans to start negotiations on a comprehensive partnership agreement (CEPA) that will see the country and the UAE deepen trade and investment ties. The UAE and Kenya are seeking to remove trade barriers on a wide range of goods and services and create opportunities for importers and exporters in both countries.

- The Bank of England hiked interest rates by 0.5% to 1.75%, the highest in 27 years. With the latest surge in gas prices, the bank expects inflation to rise above 13% at the end of the year.

Get future reports

Please provide your details below to get future reports: