Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,531 million (3.63 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar and the Sterling Pound but strengthened against the Euro to exchange at KES 135.19, KES 168.28 and KES 148.16 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 9.53% | 0.62% |

| Sterling Pound | 13.14% | 0.03% |

| Euro | 12.53% | -0.24% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate increasing from 8.53% to 8.81%, as tax remittances more than offset government payments. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 8.53% | 8.81% |

| Interbank volume (billion) | 24.63 | 14.59 |

| Commercial banks’ excess reserves (billion) | 10.40 | 22.10 |

Fixed Income

T-Bills

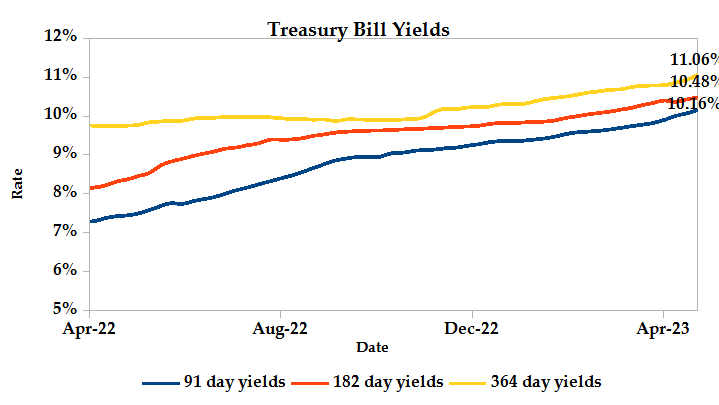

T-Bills were over-subscribed during the week, with the overall subscription rate recorded as 146.47%, up from 122.59% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 799.62% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 21.49% and 10.18% respectively. The acceptance rate increased by 1.77% to close the week at 94.67%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 33.22% from KES 8.46 billion in the previous week to KES 11.27 billion. Total bond deals increased by 7.04% from 398 in the previous week to 426.

In the primary bond market, CBK released auction results for the 3-year Treasury Bond; FXD1/2022/03, which sought to raise KES 30 billion. The issue was under-subscribed receiving bids worth KES 7.33 billion, representing a performance of 24.43%. KES 1.76 billion worth of bids were accepted at a weighted average rate of 13.47%.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average 0.38% compared to the previous week, 0.90% month to date and 2.15% year to date. The yields on the 10-Year Eurobonds for Angola and Ghana increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 2.60% | 1.78% | 0.84% |

| 2018 10-Year Issue | 2.52% | 0.84% | 0.30% |

| 2018 30-Year Issue | 1.18% | 0.62% | 0.30% |

| 2019 7-Year Issue | 2.97% | 0.72% | 0.26% |

| 2019 12-Year Issue | 1.66% | 0.79% | 0.30% |

| 2021 13-Year Issue | 1.98% | 0.66% | 0.28% |

Equities

NASI, NSE 20 and NSE 25 settled 3.33%, 1.23% and 1.80% lower compared to the previous week bringing the year to date performance to -15.31%, -4.85% and -8.61% respectively. Market capitalization lost 3.35% from the previous week to close at KES 1.68 trillion recording a year to date decline of 15.35%. The performance was driven by losses recorded by large-cap stocks such as Safaricom, EABL and KCB of 7.30%, 6.08%, and 2.80% respectively. These were however mitigated by gains recorded by NCBA, Stanbic and Equity of 5.41%, 3.39% and 1.46% respectively.

The Banking sector had shares worth KES 271M transacted which accounted for 42.93% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 21M transacted which represented 3.34% and Safaricom, with shares worth KES 315M transacted represented 49.85% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Jubilee | -4.78% | 19.21% |

| Standard Group | -13.49% | 10.78% |

| Kakuzi | -24.61% | 9.94% |

| Unga | -28.44% | 9.31% |

| Trans-Century | 1.01% | 8.70% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| B.O.C | -0.71% | -8.77% |

| Longhorn | -30.00% | -8.70% |

| NBV | 25.13% | -8.10% |

| Umeme | 86.50% | -7.31% |

| Safaricom | 31.39% | -7.30% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.51 | 0.21 | -57.84% |

| Derivatives Contracts | 7.00 | 4.00 | -42.86% |

| I-REIT Turnover (million) | 0.26 | 1.28 | 386.25% |

| I-REIT Deals | 41 | 50 | 21.95% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 8.09% | -0.10% |

| Dow Jones Industrial Average (DJI) | 2.04% | -0.23% |

| FTSE 100 (FTSE) | 4.77% | 0.54% |

| STOXX Europe 600 | 8.02% | 0.45% |

| Shanghai Composite (SSEC) | 5.93% | -1.11% |

| MSCI Emerging Markets Index | 1.89% | -1.97% |

| MSCI World Index | 8.54% | -0.09% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -1.07% | -0.58% |

| JSE All Share | 5.83% | -1.08% |

| NSE All Share (NGSE) | -0.47% | -1.06% |

| DSEI (Tanzania) | -1.20% | -0.33% |

| ALSIUG (Uganda) | -7.84% | -0.80% |

US indices ended the week lower, owing to mixed quarterly reports and disappointing results from companies including Tesla and AT&T. Additionally, banking shares from Comerica Inc and KeyCorp fell as they continue to be in focus since the Silicon Valley Bank failure last month. Investors continue to seek clarity on the interest rate path.

European indices ended the week on a positive note, as strong quarterly earnings boosted shares of SAP and EssilorLuxottica, offsetting a slump in miners. The first-quarter revenue earnings surpassed analysts’ expectations and fears of a banking crisis abated as investors look ahead to the earnings season.

Asia Pacific indices, in the past week recorded a marginal decrease. Mixed economic readings raised questions over the scope of a recovery this year, as China’s manufacturing sector continued to struggle. Asian markets trended in a flat-to-low range, with caution setting in ahead of key US economic readings. Rising interest rates and tighter monetary conditions limit capital flows into the region.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 5.72% and 5.63% lower at $77.95 and $81.75 respectively. Gold futures prices settled 1.17% lower at $1994.10.

Week’s Highlights

- The Central Bank of Kenya cancelled the issuance of the reopened FXD1/2019/15 bond. This move has deepened the government’s recent struggle to raise debt financing from the local market. On the other hand, the 3-year bond underperformed raising just 1.76 billion. The poor performance could impose pressure on the Kenya Revenue Authority by the Treasury to beat the collection targets or impose higher leverage on external financing to close the budget funding gap.

- The Kenyan government, through the National Treasury is considering using international capital markets to issue a sovereign bond before the end of the 2023-2024 fiscal year. The National Treasury has asked respected financial institutions lawfully permitted to operate in North America, Europe, the Middle East, and/or Asia, to submit Expressions of Interest for comprehensive Lead Manager services to successfully assist Kenya’s return to international capital markets.

- CPF Financial Services has received regulatory approval by the Retirement Benefits Authority to manage Tier II contributions from employers who opt of the National Social Security Fund (NSSF). This will be accomplished through the Taifa (Umbrella) Pension Fund, which offers improved benefits like post-retirement medical savings and retiree medical coverage in an effort to entice firms who choose not to participate in the Tier II NSSF.

- China’s Gross Domestic Product (GDP) grew by 4.5% in the first quarter surpassing analysts’ forecast of 4%, following the end of Covid-19 restrictions. This marks the highest growth since the first quarter of last year which stood at 3%. Industrial production and resurgence in consumption were the highest contributors towards the rebound of the economy. The Manufacturing sector continues to struggle to recover from the Covid-19 induced slowdown.

- The S&P Global US Composite PMI rose to 53.5 in April 2023, up from 52.3 in March, signalling the quickest upturn in business activity since May 2022. The rise in activity was broad-based, with the services activity growth hitting a 12-month high and manufacturing output expanding modestly but at the fastest rate since May 2022. New orders in firms increased despite a continued decline in new export orders, amid new client wins, improved customer confidence and successful marketing strategies. In addition, employment growth remained solid, while work backlogs persisted for the second month running as companies mentioned struggles finding suitable candidates and retaining staff amid rising wage costs. In terms of prices, rates of input cost and output charge inflation picked up to a three and seven-month high, respectively. Finally, business confidence rose to the second-highest since May 2022.

- In the United Kingdom, Consumer Price Index (CPI) eased to 10.1% in March 2023, down from 10.4% in February but higher than market expectations of 9.8%. The rate remained above 10% for a seventh straight period and the Bank of England’s 2% target for nearly two years, suggesting that policymakers will continue raising borrowing costs. The core inflation rate which includes energy and food remained unchanged at 6.2% in March. The annual inflation rate in the Euro Area stood at 6.9% in March 2023, down for a fifth consecutive month and its lowest level since February 2022. However, the rate remained stubbornly high and well above the European Central Bank’s target of 2.0%, as did the core index, which hit a fresh record high of 5.7%.

- The S&P Global/CIPS UK Composite PMI rose to 53.9 in April 2023 from 52.2 in March, easily beating market consensus of 52.5. The reading pointed to the fastest pace of expansion in the country’s private sector since April 2022 aided by a robust and accelerated increase in service sector output. On the other hand, manufacturing output fell for the second month running and by the most since January. Overall new orders increased at a rapid pace and job creation accelerated to a six-month high. In terms of prices, input cost inflation eased to the lowest since March 2021, while prices charged inflation increased slightly as firms sought to defend margins from rising expenses. Finally, business confidence fell but was still the second-highest since March 2022.

Get future reports

Please provide your details below to get future reports: