MONTH’S HIGHLIGHTS

- Monetary Policy Committee (MPC), raised the benchmark rate by 50 basis points to 7.5% citing high inflation for the month which has peaked at 7.1% year on year. Inflation pressure has been attributed to supply chain disruptions due to the Russia-Ukraine crisis. The MPC will closely monitor the impact of the policy measures put in place and events in the global and local markets before making any additional steps to curb looming inflation.

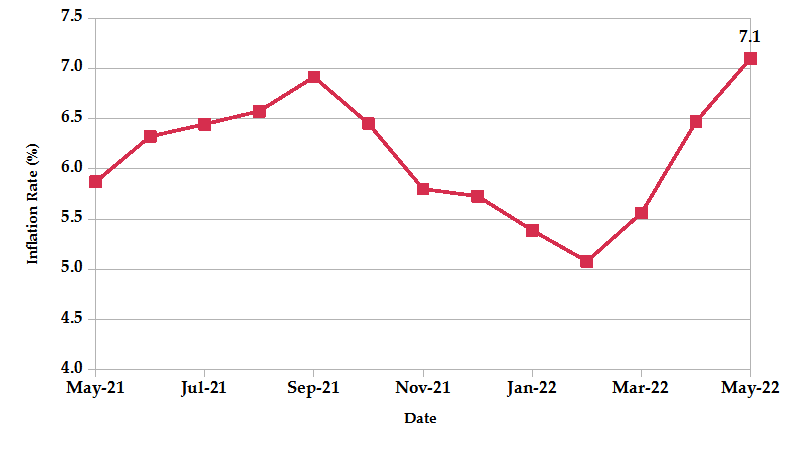

- The overall year-on-year inflation increased to 7.1% in the month of May up from 6.5% recorded in February. The increase is attributable to a rise in the price of food, housing, water, electricity, gas, fuel and transport. Supply chain disruptions as a result of the Russia-Ukraine war has caused food shortage globally. The energy and commodity sector also experienced high demand pressure as supplies continued to be insufficient.

- The East African Community (EAC) partner states reached a consensus to levy the Common External Tariff (CET) on fourth-band products capping the tax rate at 35% on imports to the EAC. Therefore, importers are expected to pay higher taxes in a move aiming at stimulating local production and industrialization.

- Stanbic Bank Kenya released the April Purchasing Managers Index (PMI) with an observed drop to 49.5 from 50.5 recorded in March on the back of high inflation, reduced output and lower new orders from clients. However, employment increased to a lesser degree than the previous month.

- Commercial banks released returns for the first quarter with most lenders registering profits compared to the same period last year. Uptake of loans has also increased as the economy rebounds as a result of the easing of COVID-19 restrictions.

- The price of wheat jumped on international markets after India banned the export to protect its local stocks.

- The Energy and Petroleum Regulatory Authority (EPRA) announced a Kshs. 5.50 increase in the pump price of petroleum products to reach a new record high. Super petrol, Diesel and Kerosene will retail at Kshs 150.12, Kshs 131 and KSHs 118.94 respectively. The increase is attributed to surging crude oil prices as observed in the 10.43% increase registered by the Free on Board of Murban oil to $93.99 per barrel. The depreciation of the shilling against the dollar has also increased the cost of importing petroleum products.

- Hass Consult released the quarter one House Price Index report. Property prices registered a 2.8% increase attributable to high inflation. Property rents also registered mild increases with satellite towns registering the highest rent increase. Additionally, Hass also released the Land Price Index which saw an overall 0.11% increase in land prices in Nairobi. Satellite towns recorded mixed performance with Thika, Juja and Ruiru registering gains while Limuru dropped.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 2.97% to stand at USD 8.18 billion(4.86 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

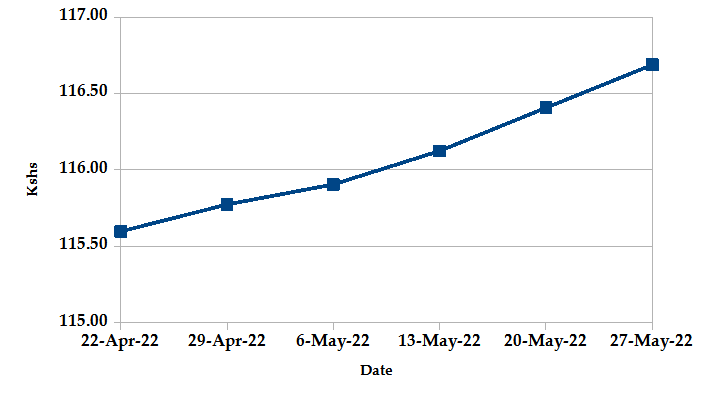

The Kenyan Shilling depreciated against the USD by 0.79%, exchanging at Kshs 116.69 at the end of the month up from Kshs 115.77 in the previous month. The depreciation is due to increased dollar demand from the oil and energy sectors. The pressure on the shilling is largely due to rising global crude oil prices and supply constraints in light of the Ukraine crisis.

USD Vs KSHS

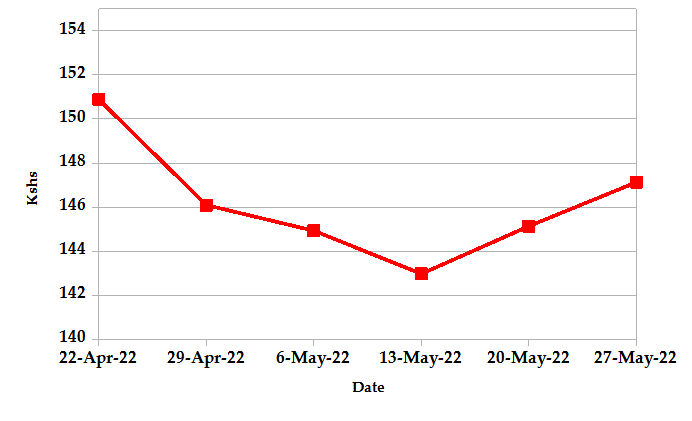

STERLING POUND Vs KSHS

Inflation

The overall year-on-year inflation increased to 7.1% in the month of May up from 6.5% recorded in February. The increase is attributable to a rise in the price of food, housing, water, electricity, gas, fuel and transport. Supply chain disruptions as a result of the Russia-Ukraine war has caused food shortage globally. The energy and commodity sector also experienced high demand pressure as supplies continue to be insufficient.

INFLATION EVOLUTION

Liquidity

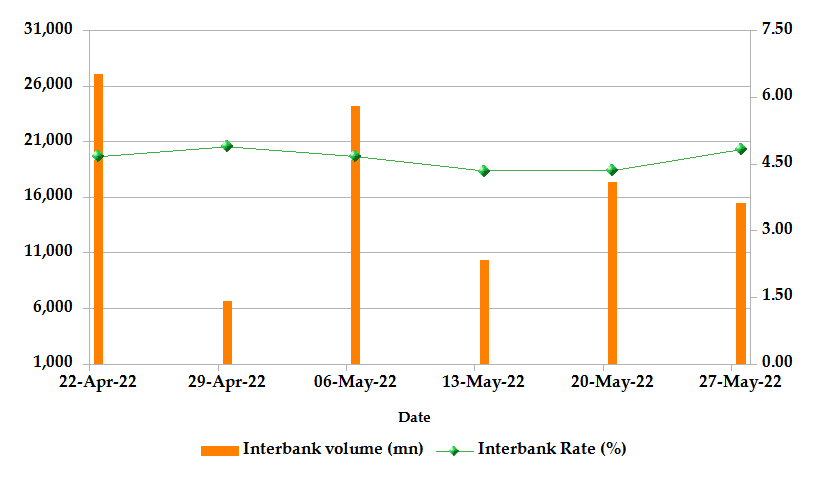

During the month, liquidity relatively eased as a result of government payments which offset tax remittances. The inter-bank rate decreased to 4.82% down from 4.89%. The volume of inter-bank transactions increased from Kshs 6.67 billion to Kshs 15.5 billion. Commercial banks’ excess reserves decreased by 40.32% to Kshs 15.10 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

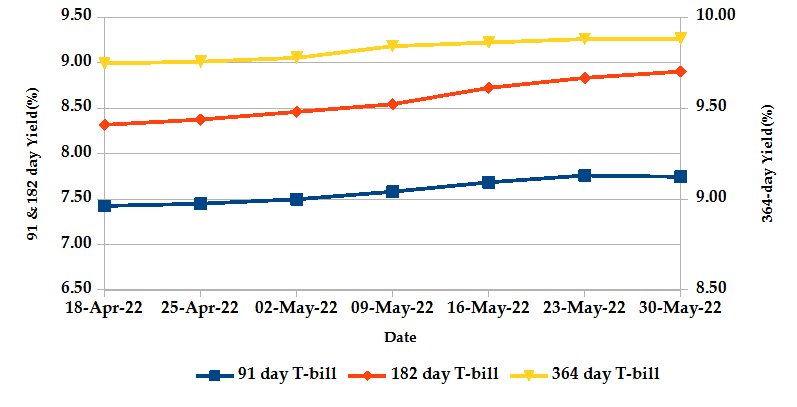

T-Bills

The T-bills recorded a slight improvement of the overall monthly subscription rate to 85.80% for the month of May, compared to 71.07% recorded in the previous month but still remained under-subscribed. The under-subscription is partly attributable to the concurrent sale of treasury bonds during the month with the Central Bank opening up a Tap sale and a new infrastructure bond. The performance of the 91-day, 182-day and 364-day papers stand at 102.8%, 61.9% and 103.1% respectively. Average yields for the 91-day 182-day and 364-day papers increased by 3.8%, 5.3% and 1.1% to 7.69%, 8.75% and 9.87% respectively.

T-BILLS

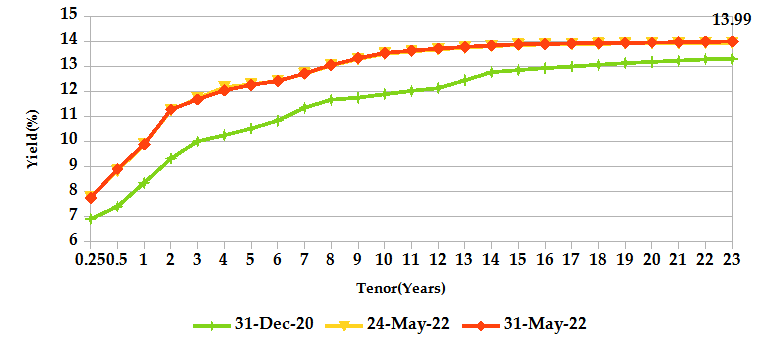

T-Bonds

T-Bonds registered a turnover of Kshs 58.57 billion from 2.066 bond deals. This represents a monthly change of 9.08% and -17.4% respectively. The yields on government securities in the secondary market were on an upward trajectory during the month of March.

In the international market, yields on Kenya’s Eurobonds declined by an average of 30.7 basis points.

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 74 contracts having a turnover of Kshs 6.06 million which was a decrease from 93 contracts having a turnover of Kshs 9.12 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.68 million with 193 deals which was an increase from Kshs 1.51 million with 218 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 91.9 million with 2 deals which was an increase from last month which recorded no ETF activity.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 6.58% | 0.64% |

| STOXX Europe 600 | 2.65% | 0.54% |

| Shanghai Composite (SSEC) | -0.52% | 2.73% |

| MSCI Emerging Market Index | 0.76% | -1.01% |

| MSCI World Index | 5.52% | 0.25% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -2.51% | -15.55% |

| JSE All Share | 4.73% | -2.43% |

| NSE All Share (NGSE) | 2.09% | 8.96% |

| DSEI (Tanzania) | 1.27% | 1.53% |

| ALSIUG (Uganda) | -0.24% | -5.51% |

- During the month, major global markets were mixed as investors continue to monitor inflation threats resulting from shortages caused by the Russia-Ukraine crisis. In the USA, the S&P 500 and Dow Jones indices gained by 0.64% and 0.54% respectively from the previous month. This follows as a better-than-expected monthly jobs report fueled investor bets on more aggressive Federal Reserve rate hikes ahead, stoking fears of slowing economic growth. However, investors’ sentiments improved as data pointing to cooling inflation and strength in the consumer renewed optimism on growth sectors. The core personal consumption expenditures rose 4.9% in the 12 months through April, slower than the 3.2% reported in the prior month.

- On a regional front, most markets declined. The FTSE ASEA Pan African index, representing the overall African markets, declined by 15.55% from the month of April. South Africa’s JSE All Share declined by 2.43%, Nigeria’s All Share Index increased by 8.96%, Tanzania’s DSEI increased by 1.53% and Uganda’s All Share Index declined by 5.51%. Tanzania announced a 3.8% inflation up from 3.6% in the previous month. South Africa, Ghana and Nigeria raised their benchmark interest rates by 50 basis points, 200 basis points and 150 basis points to new record highs of 4.75%, 19% and 13% respectively to tame inflationary fears as a result of commodity shortages in the global markets and weakening of currencies against the Dollar on the back of high demand for commodity trade. However, Rwanda retained its rate at 5%. Inflation has continued rising with South Africa depleting its fuel subsidy resulting in record-high gasoline prices in June and Tanzania Recording a Deficit of $1.31 Billion in Q1 2022 on High Import Bills.

- On the global commodities markets, oil prices rose as speculations on the exclusion of Russia from OPEC continue rising. European Union leaders agreed to a phased ban on Russian oil and as China ended its COVID-19 lockdown in Shanghai, shortages are expected as demand pressure outweighs supply. The Crude Oil WTI futures surged by 13.87% from the previous month of February. The ICE Brent Crude Oil increased in value by 8.13%.

YIELD CURVE

EQUITIES

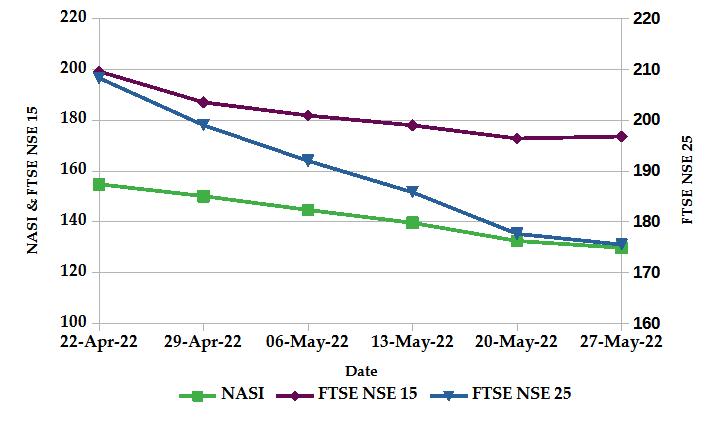

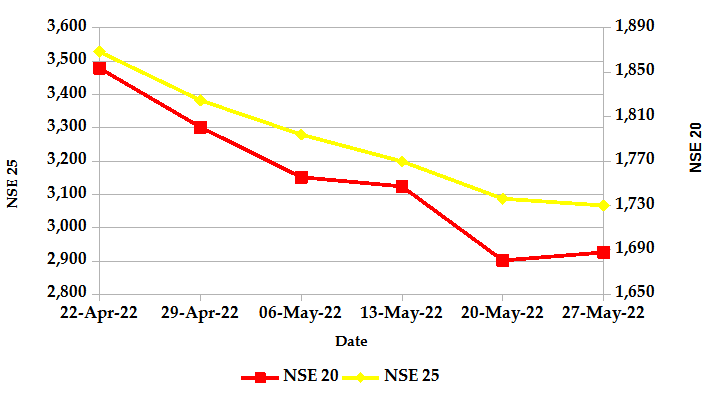

During the month of May, the market capitalization declined by 13.57% to Kshs 2.023 trillion. Total shares traded and equity turnover increased by 92.2% and 29.8% respectively to 370 million shares and Kshs 15 billion. NASI, NSE 20 and NSE 25 declined by 13.5%, 6.3% and 9.3% on a monthly basis. On a weekly basis, the NASI and NSE 25 declined by 2% and 0.7% respectively while NSE 20 increased by 0.4%. The decline in NASI is a result of the depreciation of large-cap stocks such as Kengen Company, EABL and Safaricom.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

Get future reports

Please provide your details below to get future reports: