MONTH’S HIGHLIGHTS

- Kenya’s official forex reserves dipped by KSh39 billion in August due to external loans interest payments and possible US Dollar sales into the market to stave off exchange rate volatility. During the month, the CBK was due to pay the latest semi-annual interest instalment on the KSh219.8 billion Eurobond contracted on February 22, 2018, and a nine-year, KSh137.4 billion syndicated loan that was taken up in February 2019.

- The banking industry contributed 27% of all corporate taxes paid in Kenya in 2020 and 2019 even as the adverse impact of the COVID-19 pandemic caused a 12% overall decline in their total tax contribution in 2020 compared to 2019.

- The Treasury published new regulations that give the Capital Markets Authority (CMA) powers to oversee all investment funds formally solicited from the public. This is part of an effort to rein in fraudulent and unregulated schemes.

- The Ministry of Industrialization, Trade and Enterprise Development and the Special Economic Zones (SEZ) Authority recently launched a web portal where current and potential investors will access key information such as investment opportunities and incentives, investor road maps and facilities, as well as administrative and tax incentives.

- Uganda has protested a 79 percent cut on its scheduled sugar exports to Kenya, reigniting trade disputes between the two East African Community states. A deal between the two countries allowed Uganda to export surplus sugar into the country three years ago. But Nairobi delayed the implementation until late last year when the neighbouring state was allowed to ship in 20,000 tonnes of the 90,000 tonnes surplus that it had requested.

- Asia Pacific stocks were mostly up at the close of the month even as the latest Chinese economic data disappointed. Investors now await the latest U.S. jobs report which they hope will provide clues on the Federal Reserve’s monetary policy moving forward. The Caixin services purchasing managers’ index (PMI) for August was below the 50 mark indicating growth.

- Bank of Kigali (BK Group) net profit for six months to June rose 41.5 percent on the back of increased interest and non-interest income. The profit growth signals a recovery for the publicly-traded Rwandan lender and mirrors the trend that has been seen by lenders in Kenya as the economy picks up from COVID-19 disruptions.

- Kenya and Pakistan have agreed to remove non-tariff barriers, ending a long-standing tariff war that hurt trade between the two countries. The attestation fee for Kenyan tea exports has officially been removed.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 3.80% to stand at USD 8.99 billion(5.49 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

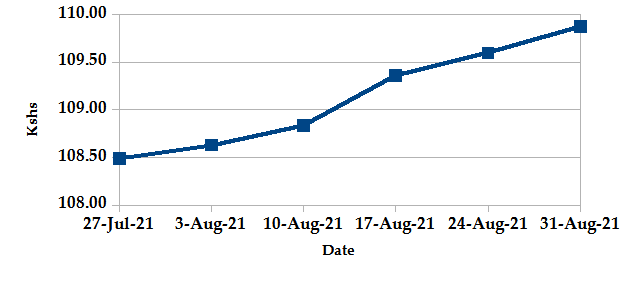

The Kenyan Shilling depreciated against the USD by 1.16%, exchanging at Kshs 109.87 at the end of the month up from Kshs 108.61 in the previous month. The depreciation is due to depressed inflows from tourism and tea amid a recovering economy which has pushed up demand for imports. The shilling continues to be pressured by a widening gap between supply and demand of the US dollar due to a faster growth in imports than exports.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

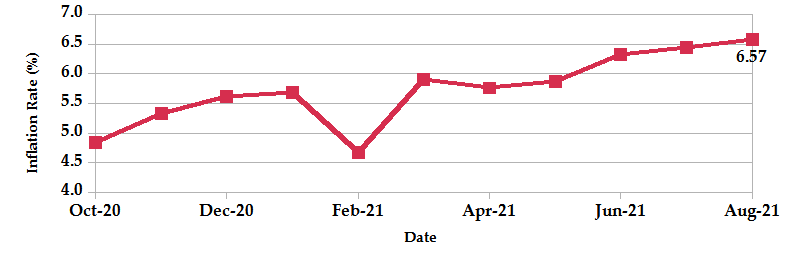

The overall year-on-year inflation increased to 6.57% in the month of August up from a revised figure of 6.44% in July. The increase is attributable to an increase in the food and non-alcoholic drinks Index by 10.67% and Transport Index increased by 7.93%. Housing, Water, Electricity, Gas and Other Fuels’ Index by 5.07%. That was fueled by an increase in cooking fuel and electricity prices and house rentals. A new value-added tax on cooking gas came into effect on July 1.

INFLATION EVOLUTION

Liquidity

During the month, liquidity decreased as a result of government payments which partly offset tax receipts. The inter-bank rate increased to 3.36% up from 3.17%. The volume of inter-bank transactions increased from Kshs 6.07 billion to Kshs 12.46 billion. Commercial banks’ excess reserves decreased to Kshs 13.20 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

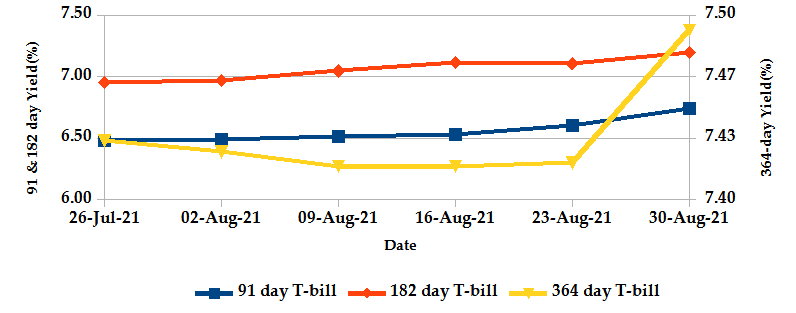

The T-bills recorded an overall subscription rate of 71.26% at the end of the month of August, compared to 101.05% recorded in the previous month. The under-subscription is partly attributable to investors’ low confidence in the market. The performance of the 91-day, 182-day and 364-day papers stand at 172.5%, 75.2% and 26.8% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 3.9%, 3.3% and 0.9% respectively to 6.74%, 7.20% and 7.49%.

T-BILLS

T-Bonds

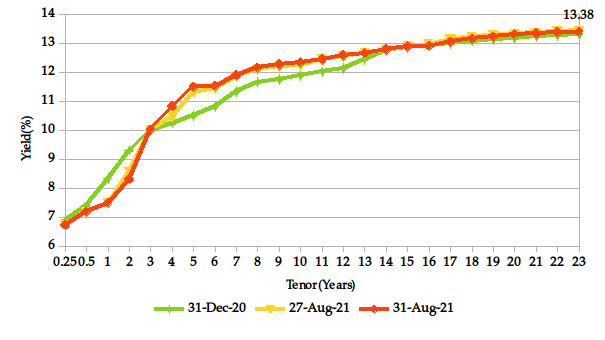

At the end of the month, the T-Bonds registered a turnover of Kshs 83.06 billion from 2,006 bond deals. This represents a monthly increase of 25.1% and a decrease of 3.0% respectively. The yields on government securities in the secondary market marginally increased during the month of August.

In the international market over the last week, yields on Kenya’s Eurobonds declined by an average of 6.35 basis points.

YIELD CURVE

EQUITIES

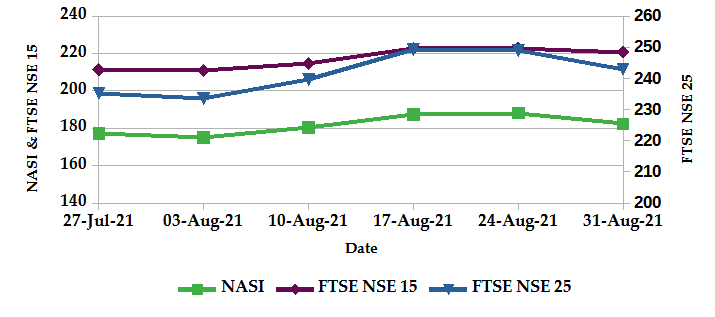

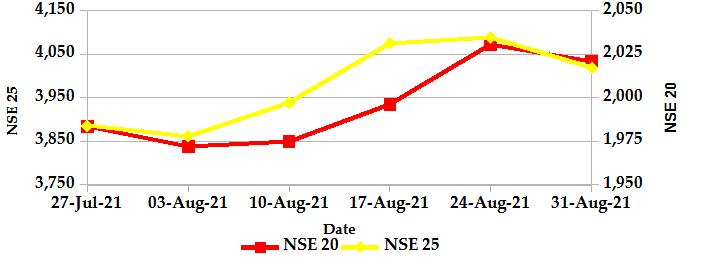

During the month of August, the market capitalization rose by 2.72% to Kshs 2.84 trillion. In addition, total shares traded and equity turnover gained by 20.3% and 37.2% respectively to 18.6 million shares and Kshs 0.79 billion. NASI, NSE 20 and NSE 25 gained by 2.7%, 2.4% and 3.3% respectively on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 declined by 3.1%, 0.5% and 1.7% respectively. The gain in NASI is a result of the appreciation of large-cap stocks such as ABSA Bank, Equity Group and Stanbic Holdings.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 254 contracts having a turnover of Kshs 40.6 million which was an increase from 214 contracts having a turnover of Kshs 14.1 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 11.4 million with 224 deals which was an increase from Kshs 2.1 million with 231 deals recorded over the last month.

- The ETF market over the month recorded no activity over the month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 0.81% | 2.90% |

| STOXX Europe 600 | -0.19% | 1.98% |

| Shanghai Composite (SSEC) | 0.84% | 4.31% |

| MSCI Emerging Market Index | 3.04% | 2.42% |

| MSCI World Index | 0.62% | 2.35% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 0.01% | 2.06% |

| JSE All Share | -0.23% | -2.88% |

| NSE All Share (NGSE) | -0.61% | 1.74% |

| DSEI (Tanzania) | 0.20% | -0.20% |

| ALSIUG (Uganda) | 0.64% | 3.22% |

- U.S. stock markets made significant gains, shrugging off concerns about a slowing economy, spreading COVID-19 and a hurricane lashing New York City. The Labor Department noted that initial jobless claims fell to a new post-pandemic low suggesting that the latest wave of Covid-19 in the U.S. is still not triggering higher lay-offs. In the USA, the S&P 500 and Dow Jones indices gained by 2.90% and 1.21% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 appreciated by 1.98% and 1.24% respectively due to positive investor sentiment from the speech by Fed Chair Jerome Powell in which he said tapering of stimulus measures could begin this year. He added the central bank would remain cautious.

- On a regional front, a key milestone was reported in the ongoing geothermal drilling contract in Ethiopia. Ethiopia Electric Power Company projects it will complete the drilling of the first well within two months. The FTSE ASEA Pan African index, representing the overall African markets, gained by 2.06% from the month of July. Nigeria’s All Share Index rose by 1.74% and Uganda’s All Share Index increased by 3.22%. However, South Africa’s JSE All Share declined by 2.88% and Tanzania’s DSEI declined by 0.22%.

- On the global commodities markets, oil prices fell overnight as OPEC+ agreed to increase global oil production by 400,000 barrels per day (bpd). Additionally, the group revised their consumption forecasts to swing to a production surplus of 2.5 million bpd in 2022. The Crude Oil WTI futures and the ICE Brent Crude Oil plunged by 7.37% and 4.38% from the previous month of July.

Get future reports

Please provide your details below to get future reports: