MONTH’S HIGHLIGHTS

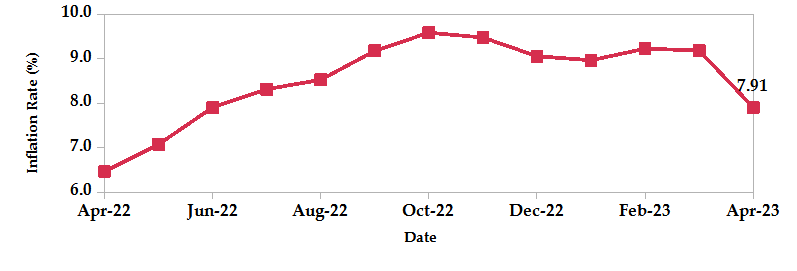

- Inflation significantly declined to 7.91% in April 2023 from 9.19% in March 2023, mainly driven by lower costs of food prices as supply improved amid cooler weather conditions. Food and non-alcoholic beverages prices declined to 10.1% in April from 13.4% in March, reflecting lower prices of edible oils. The housing, water, electricity, gas and other fuels category edged 2.7% higher as a result of increased electricity prices. The transport index rose 0.2% despite unchanged petrol prices.

- The Kenyan government, through the National Treasury, is considering floating a Sovereign bond in international capital markets before the end of the fiscal year 2023/2024. The National Treasury has requested credible financial institutions authorized to operate in North America, Europe, the Middle East, and/or Asia submit Expressions of Interest for Lead Manager services that will effectively assist the country’s re-entry into international debt markets. This is expected to offset upcoming Eurobond maturities as the country’s debt repayment and distress pressures rise.

- The IMF’s World Economic Outlook for April 2023, projects that the global output growth is expected to decrease from an estimated 3.4% in 2022 to 2.8% in 2023, before experiencing a slight increase to 3.0% in 2024. The outlook for the global economy is predominantly negative, with significant risks, particularly regarding the financial sector, as vulnerabilities in the banking industry become more apparent. Meanwhile, Kenya’s growth outlook is positive, with an upward revision from the October 2022 forecast of 5.1% to 5.3% in 2023, and a moderate acceleration to 5.4% in 2024.

- The Retirement Benefits Authority (RBA) has granted regulatory approval to CPF Financial Services and Enwealth Financial Services to handle Tier II contributions from employers who opt out of the National Social Security Fund (NSSF). The Taifa (Umbrella) Pension Fund and the Enwealth Umbrella Fund will respectively be used by CPF Financial Services and Enwealth Financial Services to manage these contributions.

- The Capital Markets Authority (CMA) has proposed a significant reduction in the minimum investment threshold for professional investors in restricted real estate investment trusts (REITs) from Kshs 5 million to Kshs 10,000. This proposal is aimed at boosting investor interest in REITs and supporting the government’s affordable housing agenda.

- The Central Bank of Kenya in collaboration with the financial industry has upgraded the Kenya Payment and Settlement System (KEPSS) to the ISO 20022 standards as part of the National Payment Strategy 2022-2025. KEPSS is a Real Time Gross Settlement System (RTGS) which ensures that transactions are cleared and settled continuously. The adoption of ISO 20022 embeds richer data on financial messages, enhancing the accuracy of trading parties and providing insights into customer preferences.

- The Eurozone inflation rate slightly increased to 7.0% in April from 6.9% in March, a rate that is significantly higher than the European Central Bank’s target of 2.0%. Energy prices edged 2.5% higher, but service prices rose at an accelerated 5.2%. Food, alcohol & tobacco inflation dropped to 13.6% in April from 15.5% the previous month. Non-energy industrial goods inflation fell to 6.2% in April from 6.6% the previous month. Consumer prices grew 0.7% on a monthly basis, the third month in a row.

- The US S&P Global Manufacturing PMI was adjusted downwards to 50.2 in April 2023, falling short of the preliminary reading of 50.4 and compared to 49.2 in March. The reduction is ascribed to the contraction of export orders and the resurgence of new orders into the expansion territory, as well as the hastened growth in production since May 2022. On the other hand, the S&P Global/CIPS UK Manufacturing PMI was revised upwards to 47.8 in April, surpassing the initial estimate of 46.6, but still indicating a continuing downturn in the UK manufacturing sector for a ninth straight month, as compared to 47.9 in March.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves increased by 1.28% to settle at USD 6.51 billion (3.62 months of import cover). This lies below CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

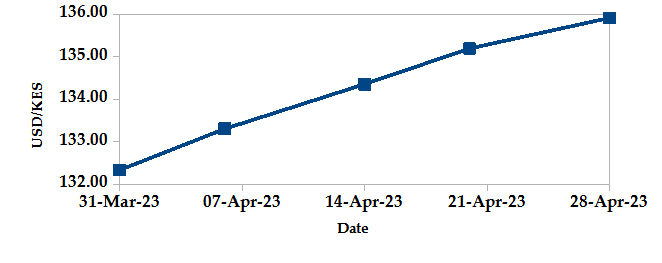

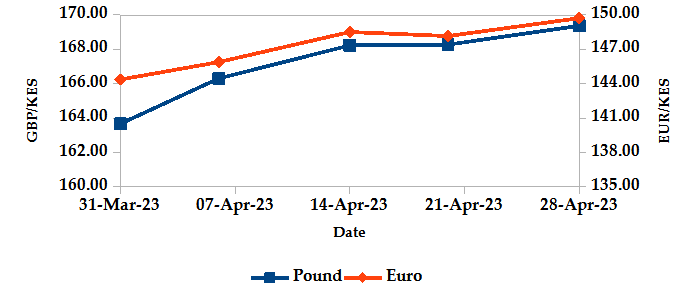

The Kenyan Shilling depreciated against the USD by 2.70%, exchanging at Kshs 135.91 at the end of the month, up from Kshs 132.33 in the previous month. The Shilling also depreciated against the Sterling Pound by 3.48% and the Euro by 3.71%, exchanging at Kshs 169.37 and Kshs 149.72 at the end of the month, up from Kshs 163.67 and Kshs 144.37 respectively in the previous month. The depreciation is due to increased Dollar demand by importers as well as investors hedging their exposure by holding foreign currency deposits.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation declined significantly to 7.91% in April from a revised figure of 9.19% in March. This is mainly attributed to lower food prices as the long rainy season prevails in the country.

INFLATION EVOLUTION

Liquidity

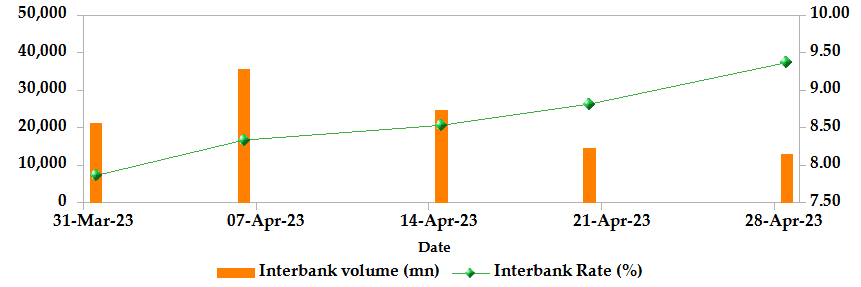

During the month, liquidity tightened as a result of tax remittances which more than offset government payments. The interbank rate rose to 9.37% from 7.86%. The volume of inter-bank transactions decreased to Kshs 12.87 billion from Kshs 21.35 billion. Commercial banks excess reserves increased from Kshs 8.90 billion to Kshs 22.10 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

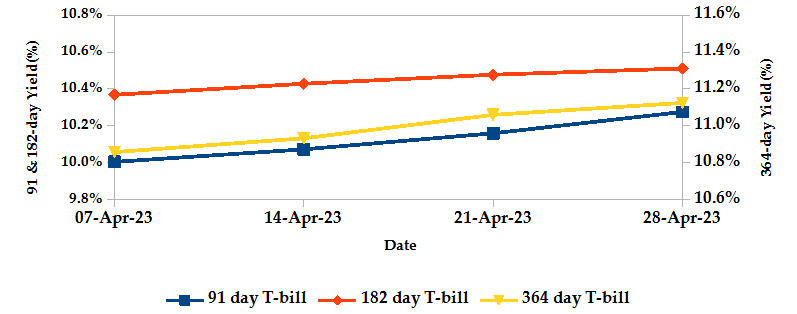

T-bills recorded an overall subscription rate of 110.33% during the month of April, compared to 97.99% recorded in the previous month. The rise in subscriptions was driven by investors flocking to T-bills, particularly the 91-day paper whose preference and dominance remained evident, as they sought to take advantage of their attractive yields. The performance of the 91-day, 182-day and 364-day papers stood at 558.01%, 15.18% and 26.41% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 3.71%, 1.08% and 3.00% to 10.28%, 10.51% and 11.12% respectively as investors aggressively bid to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

T-Bonds

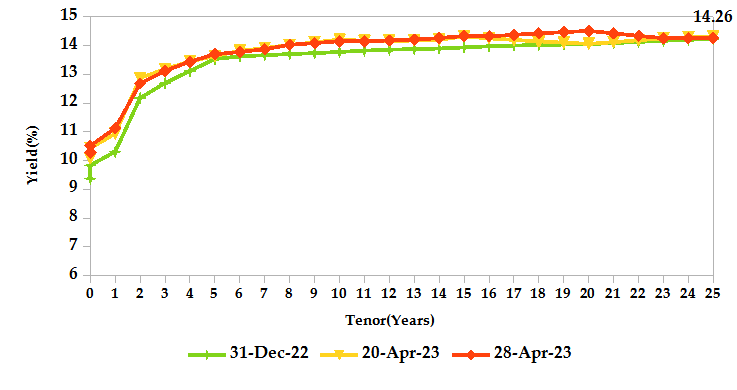

During the month, T-Bonds registered a total turnover of Kshs 38.69 billion from 1,727 bond deals. This represents a monthly decrease of 48.39% and 54.62% respectively. The yields on government securities in the secondary market increased during the month of April.

In the primary market, CBK reopened the 17-year amortized infrastructure bond; IFB1/2023/017 through a tap sale seeking to raise 10.0 billion. Additionally, Central Bank issued a new 3-year fixed coupon treasury bond; FXD1/2023/003 targeting 20.0 billion with a market-determined coupon rate.

In the international market, yields on Kenya’s Eurobonds increased by an average of 241 basis points.

YIELD CURVE

EQUITIES

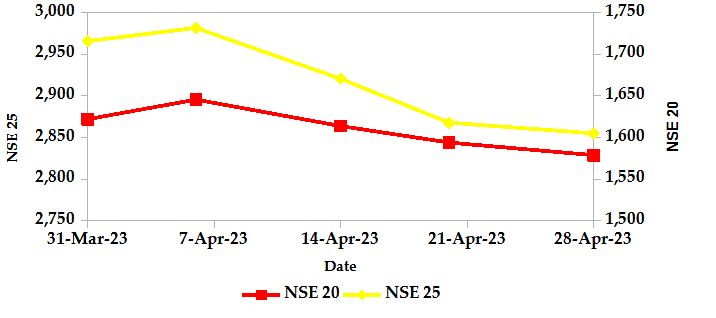

During the month, market capitalization lost 4.56% to settle at Kshs 1.68 trillion. Total shares traded declined by 67.15% to 198.06 million shares while equity turnover dropped 87.17% to close at Kshs 4.21 billion. On a monthly basis, NASI, NSE 20 and NSE 25 settled 4.55%, 2.66% and 3.74% lower. The performance was a result of losses recorded by large-cap stocks such as Standard Chartered, Safaricom and KCB of 12.35%, 8.84% and 7.46%. These were however bolstered by gains recorded by other large-cap stocks such as Co-operative and Equity of 1.14% and 0.66% respectively.

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market, over the month, recorded 22 contracts with a turnover of Kshs 1.30 million which was a decrease from 90 contracts with a turnover of Kshs 11.36 million recorded in the previous month.

- I-REIT market, over the month, recorded a turnover of Kshs 3.47 million with 220 deals which was a decrease from Kshs 7.15 million with 247 deals recorded in the previous month.

- The ETF market, over the month, recorded a turnover of Kshs 1.52 million with 2 deals which was an increase from no activity recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 1.46% | 9.03% |

| STOXX Europe 600 | 1.92% | 7.48% |

| Shanghai Composite(SSEC) | 1.54% | 6.63% |

| MSCI Emerging Market Index | -1.34% | 1.50% |

| MSCI World | 1.59% | 9.04% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 1.18% | -0.36% |

| JSE All Share | 2.96% | 6.18% |

| NSE All Share (NGSE) | -4.47% | 1.57% |

| DSEI (Tanzania) | 0.15% | -1.17% |

| ALSIUG (Uganda) | -2.77% | -8.13% |

- During the month, global markets generally recorded a positive performance. In the US, the S&P 500 and Dow Jones indices edged 1.46% and 2.48% higher respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 were up by 1.92% and 3.13%, after strong earnings from tech-related companies helped investors look past signs of economic weakness in the US.

- On a regional front, markets posted mixed performance. The FTSE ASEA Pan African index, representing the overall African markets gained 1.18% from March. South Africa’s JSE All Share and Tanzania’s DSEI gained 2.96% and 0.15% while Nigeria’s All Share Index and Uganda’s All Share Index lost 4.47% and 2.77% respectively.

- On the global commodities markets, oil future indices remained volatile, owing to an unexpected decline in Chinese manufacturing activity, which raised concerns about deteriorating economic conditions. Additionally, potential interest rate hikes by major central banks which could affect energy demand contributed to this volatility. Crude Oil WTI futures settled 1.47% higher while ICE Brent Crude Oil settled 0.29% lower to close at $76.78 and $79.54 respectively.

Get future reports

Please provide your details below to get future reports: