MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) met on May 27, 2020, against a backdrop of the continuing global COVID-19 (coronavirus) pandemic, and measures taken by authorities around the world to contain its spread and impact. The Committee noted that the policy measures adopted in March and April were having the intended effect on the economy, and are still being transmitted. The MPC concluded that the current accommodative monetary policy stance remains appropriate, and therefore decided to retain the Central Bank Rate (CBR) at 7.00%.

- During the month, key financial institutions released their Q1, 2020 financial results. ABSA Bank Kenya reported an increase in core earnings per share (EPS) from Kshs 0.39 in Q1 2019 to Kshs 0.46. Equity Group’s core EPS declined by 14.1% to Kshs 1.64, I&M Holdings’ core EPS decreased by 29.7% to Kshs 2.0, Standard Chartered Bank Kenya’s core EPS dipped by 16.6% to settle at Kshs 5.9%, HF Group reported a loss per share of Kshs 0.016 up from a loss of Kshs 3.6 per share in Q1 2019. KCB Group recorded an increase of 8.4% in core EPS to Kshs 1.95, Co-operative Bank’s core EPS fell by 0.3% to Kshs 0.612, Diamond Trust Bank’s core EPS climbed by 3.7% to Kshs 7.3% while NCBA Group’s core EPS shrunk by 26.8% to Kshs 2.3% from q1,2019.

- The International Monetary Fund (IMF) excluded Kenya from the list of countries granted loan interest payment waivers because Kenya’s per capita income stands at USD 1,710. The IMF was granting a reprieve to countries with per capita income below USD 1,215. IMF loan to Kenya stood at Kshs 50.9 billion in June 2019, representing 5.27% of the Kshs 947.5 billion Kenya owes multilateral lenders.

- Global rating agency Moody’s changed the outlook of local hostel developer Acorn Group’s Kshs 5 billion green bonds to negative from stable. Moody’s stated the negative outlook reflects the challenges posed to the construction and marketing of its assets because of COVID-19 lock-down measures and the potential longer-term impact on demand. The bond sale in October 2019 achieved an 85% subscription of the targeted Kshs 5

billion. - Global credit rating agency, Moody’s released its rating outlook where it changed Kenya’s sovereign credit outlook to “negative”, from a previous outlook of “stable”, and also affirmed the B2 credit rating. The agency pointed out that the negative outlook was a result of rising financial risks brought about by the country’s large borrowing requirements, especially during this time when the fiscal outlook is deteriorating given the erosion of the revenue base and the high debt and interest burden.

- The Central Bank of Kenya (CBK) sought to switch T-Bill investors to bonds with a view to provide relief to the exchequer’s upcoming redemptions on local debt. The desired switch has been pinned on its June infrastructure bond issue whose eligibility has been specified to holders of a one-year T-bill maturing on 1st June. The bond aims to raise Kshs 25.6 billion and has a value date equivalent to the maturity of the one-year paper tagged 2236/364 which raised Kshs 23.5 billion in proceeds. The government is presently facing debt-refinancing pressures as COVID-19 has impacted revenue generation.

- Following the amendment to the Retirement Benefits Act, the treasury Secretary published draft regulations showing rules and limits for accessing pension savings for home purchase. The changes to the law will allow workers to use up to Kshs 7 million or a maximum of 40% of their retirement savings to buy their first residential houses boosting home ownership and lifting the sluggish property market. Trustees of the various retirement schemes will lay out the rules to be followed before one can access their pension to fund their home purchase.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves improved by 7.58% to settle at USD 8.33 billion(4.99 months of import cover). This meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

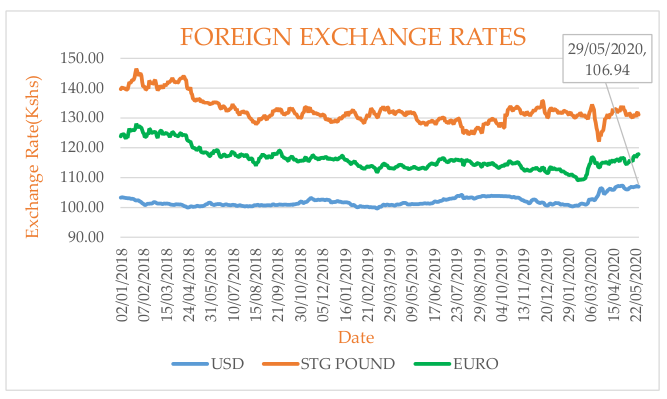

Currency

The Kenyan Shilling remained relatively stable against major global currencies. It appreciated by 0.32% against the USD to trade at Kshs 106.94, from Kshs 107.29 registered at the end of April. The gains recorded is due to increase in foreign exchange reserves after the CBK received USD 750m from the International Monetary Fund(IMF) for economic support.

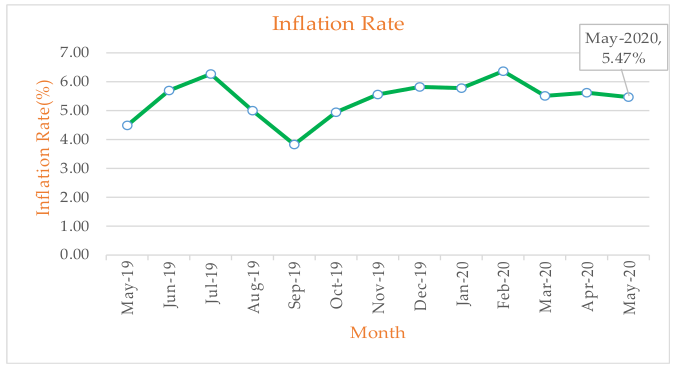

Inflation

The overall year on year inflation decreased to 5.47% in the month of May down from 5.62% in April. The change is attributable a high base effect which offset 0.86% increase in Food and Non-Alcoholic Drinks’ Index , 0.84% rise in Housing, Water, Electricity, Gas and Other Fuels’ Index, and 0.02% appreciation in the Transport Index. The increase in Transport Index was recorded despite decrease in prices of petrol and diesel by 9.81% and 19.12%, respectively.

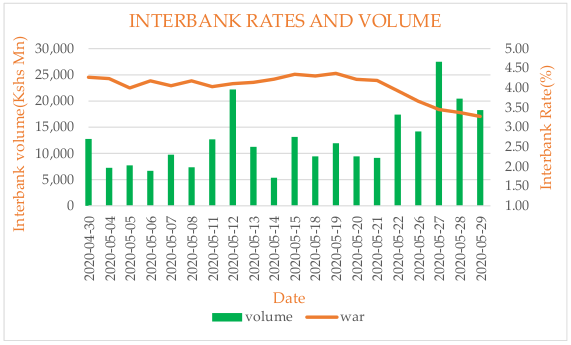

Liquidity

During the month, liquidity improved with the inter-bank rate closing at 3.44% in the month of May down from 4.27% in April. This is mainly as a result of government payments and tax refunds done during the month, and the reduction of the Cash Reserve Ratio (CRR) to 4.25%. The commercial banks excess reserves stand at Kshs.35.20bn down from Kshs.42.7bn in April. The volume of inter-bank transaction increased from Kshs 12.78bn to Kshs.18.25bn.

FIXED INCOME

T-Bills

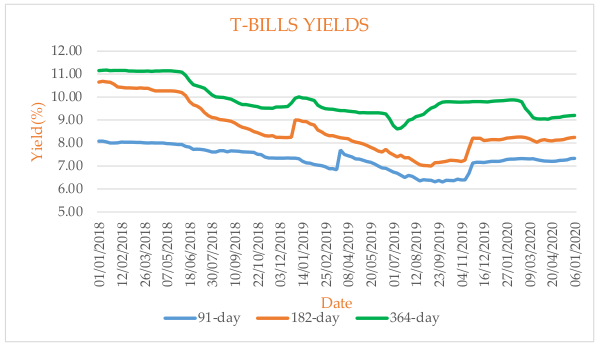

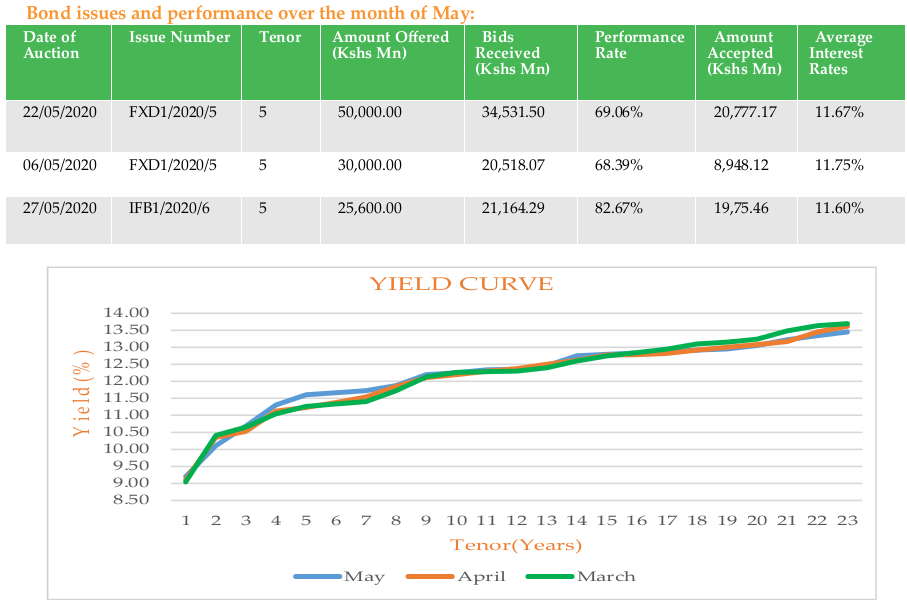

The T-bills recorded an overall subscription rate of 103.7% during the month of May, compared to 72.8% recorded in the previous month. The over-subscription is attributable to high liquidity in the money market. The subscription rates for the 91-day, 182-day and 364-day paper rose to 151.3%, 61.5% and 126.8%, respectively, from the 86.8%, 28.4% and 111.7% recorded in April. The yields on the 91-day, 182-day and 364-day papers increased by 126, 140 and 91 basis points respectively, to settle at 7.33%, 8.25% and 9.20%.

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs.13.74bn from 456 bond deals. This represents a weekly increase of 33.06% and 9.62% respectively. The yields on 4-year, 5-year, 6-year, and 7-year government securities in the secondary market increased in the month of May from April. On the other hand, towards the end of the curve, May had reduced yields compared to April. In the international market, yields on Kenya’s Euro-bonds remained stable, edging up by an average of 5.4 basis points. The yields on the 10-year Euro-bonds for Angola and Ghana also remained fairly stable.

Equities

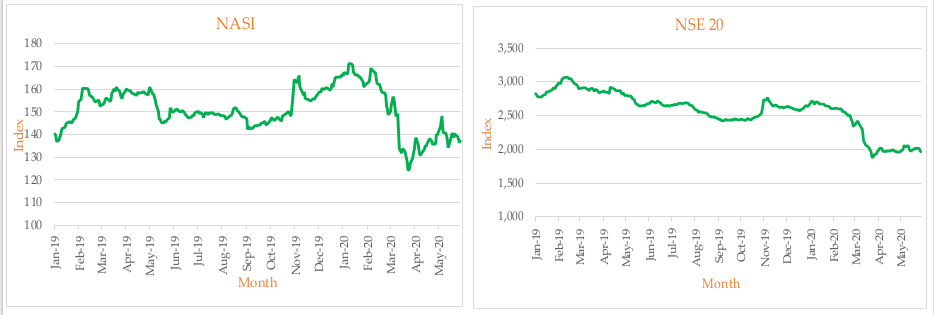

During the month of April, the market capitalization fell by 1.83% to Kshs 2.10 trillion down from Kshs 2.14 trillion. However, total shares traded and equity turnover rose by 23.22% and 47.81%, respectively to 84 million shares and Kshs 2.37 billion. NASI, NSE 20 and NSE 25 declined by 1.83%, 0.51% and 2.69%. The equity market performance during the month was driven by losses recorded by large cap stocks such as Diamond Trust Bank (DTBK), Standard Chartered Bank, Equity Group and EABL, of 14.2%, 11.5%, 6.4% and 6.2%, respectively.

ALTERNATIVE INVESTMENTS

- During the month of May, the derivatives market recorded a turnover of Kshs 2.04m with three unit deals executed. The I-REIT market registered a turnover of Kshs 7.88m from a total of 86 unit deals. The ETF market closed the month with a turnover of Kshs 4.41m resulting from a total of 2 unit deals.

- During the month, the following real estate-related reports were released; Hass Property Index Q1’2020 report by Hass Consult, the Land Price Index Q1’2020 Report by Hass Consult, and Housing Price Index Q1’2020 report by the Kenyan Bankers Association (KBA). The key insights derived from these reports indicate that land prices have declined marginally by 0.9% and 0.2% for suburbs and satellite towns, respectively, during Q1’2020. House prices contracted by 0.5% in Q1’2020, 0.1% points lower than the 0.6% recorded in Q4’2019. Townhouses accounted for 45.0% of the units sold during the quarter while apartments, bungalows and maisonettes accounted for 33.0%, 12.0% and 10.0%, respectively. Detached units and apartments recorded an average y/y price correction of 1.6% and 2.0%, respectively, and a 1.3% q/q appreciation for detached units and a 0.4% correction for apartments.

GLOBAL AND REGIONAL MARKETS

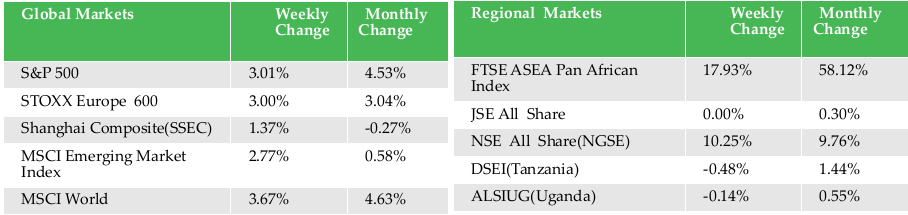

- During the month, major global indices were on the rise except China’s SSEC which fell by 0.27%. The World MSCI Index soared by 4.63% while the MSCI Emerging Markets Index rose marginally by 0.58%. USA’s DJI and S&P 500 edged higher by 4.26% and 4.53% respectively despite prevalent US-China tensions. In Europe, the European index, STOXX Europe 600 edged up by 3.04% while UK’S FTSE 1000 climbed up by a margin of 2.97%.

- On the regional front, the Pan African index FTSE ASEA registered a monthly gain of 58.21% from the previous month of April. South Africa’s JALSH gained by 0.30%, Nigeria’s NGSE Index went up by 9.76%, Tanzania’s DSEI improved by 144 basis points with Uganda’s ALSIUG rising marginally 55 basis points.

- On the global commodities market, oil futures recovered sharply from losses recorded in the month of April. Crude Oil WTI and ICE Brent Crude oil appreciated by 88.38% and 39.81%, respectively. On a weekly basis, the oil futures increased by 6.74% and 0.57% respectively. The gold futures prices have remained relatively unchanged on a weekly basis but rose by 2.52% on a monthly perspective.

Get future reports

Please provide your details below to get future reports: